LVMH takes Tiffany & Co. off the market with a $16.6bn sparkling diamond ring.

Blog 6 - 1/12/2019

This week’s blog is going to consider mergers and acquisitions and the steps that lead to a successful deal being made. Valuation of a company within a merger or acquisition is essential and can often determine the viable success of the companies once they become one entity or once they have shared ownership. ‘It is tradition to gush at engagements. Luxury group LVMH did not hold back as it put a $16.6bn ring on Tiffany on Monday.’ (Lex, 2019) .

Louis Vuitton Moët Hennessy (LVMH) are a luxury goods conglomerate, Bernard Arnault is the CEO whom is also known for being the majority shareholder in Christian Dior. Christian Dior SE is the majority shareholder of LVMH owning 40.9% and have 59.01% of the voting rights, LVMH is the world’s largest luxury group by revenues, and in 2018 had sales of €46.8bn, which is almost triple what its competitor Kering (Agnew, 2019) . LVMH’s success is deeply rooted into Bernard Arnault’s ability to acquire new firms and expand into new sectors, making LVMH’s portfolio truly diverse (Agnew, 2019) . LVMH have had a number of huge successes, however one notable loss was that of Hermès, where Bernard used derivative contracts with different banks to secretly invest until he had 17% of shares in the company when they eventually found out that this had been LVMH investing the entire time, this issue was then taken to court and Mr Arnault was forced to sell his shares due to claims it was a form of corporate assault, however he still was able to make money from this as the share price of Hermès had increased and he ended up selling out at the perfect time (Agnew, 2019) . From this we can infer the intent that Mr Arnault has when it comes to expanding his brand and going after the company’s he wants relentlessly.

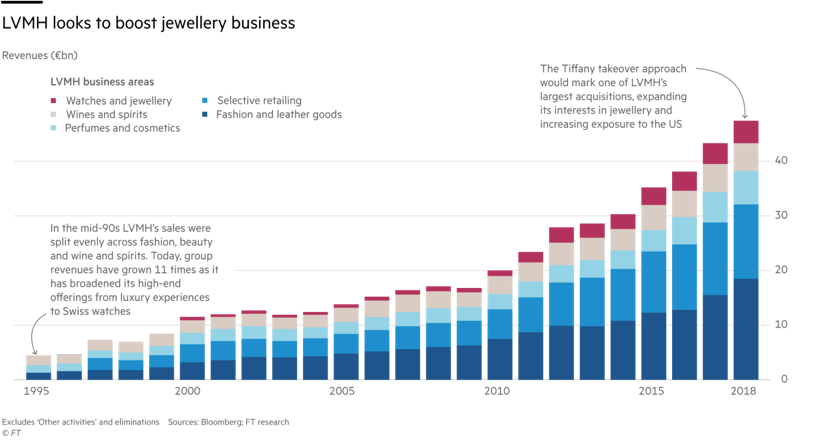

LVMH recently announced that they wished to acquire Tiffany to enable them to expose themselves to the US market, as well as expanding further into the jewellery sector. As per the graph below, you can see the increase in revenues in each sector in relation to luxury goods. The acquisition of Tiffany would lead the company to greater strengths, opening the French firm, LVMH, to not only the US market but also to the vast consumer base that Tiffany holds (White, 2019) .

The graph pictured below was taken from a Bloomberg article published on the 21stNovember that stated that the offer of $130 per share was close to a deal that Tiffany may accept however not necessarily enough. (Torsoli, 2019) . The all-time high share price in 2018 was $140 and so offering $130 per share to acquire Tiffany, for some people did not seem a sufficient offer. Not forgetting to mention LVMH originally approached Tiffany with a $120 per share offer, so you can see the fight from LVMH to acquire this company. When calculating its ebitda multiple value when offering $120 per share was at meagre ratio of 14 times, compared to the more generous ebitda ratio of 22 times that LVMH paid out for Bulgari in 2011 (Lex, 2019) . Cedric Ozazman who is the head of investment and portfolio management at Reyl & Cie stated that considering the multiples that LVMH had paid out for Bulgari, then a minimum expected offer per share should be $140 to $145 (Torsoli, 2019) . However, now reported on the 25thNovember as I write this blog, the acquisition has been agreed at a price of $135 per share (White, 2019) . ‘The $135 price tag represents a 7.5% premium over Tiffany’s closing share level on Friday, and is more than 50% higher than where the stock price stood before LVMH’s interest emerged.’ (White, 2019) . Mr Ozazman also said that Tiffany’s current Ebitda margin ‘Seems stuck in the 22%-25% meaning that it is close to peak margins and so there are little expansion prospects’, however for LMVH this is the perfect company to acquire, despite the little room for expansion with Tiffany as a company alone, once combined with his brand portfolio, it’s the perfect acquisition target for LVMH (Torsoli, 2019) .

Interestingly, since the announcement of the agreed deal on the 25thNovember 2019, we can see a +9.50 on LVMH’s share price, and also a +7.74 on Tiffany’s share price, clearly a successfully announced acquisition! (Yahoo Finance , 2019) .

So the question is why Tiffany and why now?

LVMH is buying Tiffany for what is equivalent to an equity value of $16.2bn, or as agreed $135 per share, and it makes a great deal of sense on paper (Sozzi, 2019) . Tiffany has had difficult trading circumstances with lower spending and it soon fell of the list of top-tier brands, however for LVMH it is an opportune way to enter the jewellery and watch market and they seem to have long-term prospects for the company, any way to diversify LVMH into sectors they don’t currently dominate and they seem particularly keen. However, often M&A’s are undertaken for the sake of Brand value opposed to the actual capital value of the company, for example in the academic journal: Financial Value of Brands in Mergers and Acquisitions: Is Value in the Eye of the Beholder? They state that firms paid significant prices to acquire targeted brands. In a watershed transaction, Philip Morris acquired Kraft for $12.9 billion, four times its book value. Reflecting on the premium paid, Philip Morris chief executive officer (CEO) Hamish Marshall concluded, “The future of consumer marketing belongs to the companies with the strongest brands” (Bahadir, Bharadwaj, & Srivastava, 2008) . As far back as 1989 the ICAEW were labelling Brand Valuation “is potentially corrosive to the whole basis of financial reporting” as they argued that balance sheets do not purport to be statements of value. Taking this theory further, it’s potential that companies no longer necessarily value a company based purely on actual financial reporting, and that brand value and a brand name can be equally as valuable from the eye of an acquiring company, and as the theory states, can value really be in the eye of the beholder? For LVMH Tiffany is the perfect firm to acquire to balance and improve its portfolio, and so its value to LVMH is well worth the $16.2bn equity value.

(White, 2019) . But in regards to its actual market benefits of adding Tiffany to its brand portfolio, it increases its presence in the jewellery market to 18.4%. For LVMH, the value isn't only based upon its share price, but upon its brand and its added value it can bring to the company once acquired.

List of references

Agnew, H. (2019, November 1). How one franc turned LVMH into the world’s largest luxury group . Retrieved from Financial Times : https://www.ft.com/content/c79eccfc-fca1-11e9-a354-36acbbb0d9b6

Bahadir, S. C., Bharadwaj, S. G., & Srivastava, R. K. (2008). Financial Value of Brands in Mergers and Acquisitions: Is Value in the Eye of the Beholder?Retrieved from Journal of Marketing : Financial Value of Brands in Mergers and Acquisitions: Is Value in the Eye of the Beholder?

Lex. (2019, November 25). LVMH/Tiffany: diamond geezer. Retrieved from Financial Times: https://www.ft.com/content/7753ac63-c686-4dc8-9b19-6c17a00679a2

Sozzi, B. (2019, November 25). Merger Monday roars back - LVMH buys Tiffany, Charles Schwab buys TD Ameritrade. Retrieved from Yahoo Finance: https://finance.yahoo.com/news/merger-monday-has-roared-back-lvmh-buys-tiffany-charles-schwab-buys-tdameritrade-132024123.html

Torsoli, A. (2019, November 21). LVMH's New $16 Billion Offer for Tiffany May Still Be Too Low for Some. Retrieved from Bloomberg: https://uk.finance.yahoo.com/news/lvmh-16-billion-offer-tiffany-120608376.html

White, S. (2019, November 25). LVMH to buy U.S. jeweller Tiffany for $16.2 billion. Retrieved from Reuters: https://uk.reuters.com/article/uk-tiffany-m-a-lvmh/lvmh-to-buy-u-s-jeweller-tiffany-for-16-2-billion-idUKKBN1XZ0KB

Yahoo Finance . (2019). Tiffany & Co (TIF). Retrieved from Yahoo Finance: https://uk.finance.yahoo.com/quote/TIF?p=TIF&.tsrc=fin-srch

Great read Emily, do you think the overall value of the company lies within its brand value or financial position?

ReplyDeleteThank you for your comment Eleanor! It often depends on the type of investor which is considering the company, a profitable company is always favourable! However, brand value can be instrumental in a company's potential, having repeat custom and a loyal customer base can mean a company may have more opportunities for +NPV projects which can lead to higher profitability in the future.

DeleteI would say that a combination of the two would be the most desired, although often investors take a low profit company with high brand value and manage to make profits through new investments. Brand value should never be undervalued!